FDI in the Netherlands: a transaction essential

In the Netherlands, the Investment Screening Bureau (Bureau Toetsing Investeringen, BTI), responsible for FDI enforcement, has been steadily handling more cases since the Vifo Act entered into force. According to its Dutch-language annual report, in 2025 the vast majority of investments were cleared unconditionally, with only a handful being subject to conditions. Just one prohibition was issued, which arrived after the period of the annual report (see Solvinity below). Yet the high clearance rate does not mean the Vifo Act has little impact on transactions. In practice, most friction is invisible in the statistics. Factors that discourage deals include scope uncertainty, review duration (up to 176 days in 2025), and the fact that even limited partners in investment funds without control rights may be forced to identify themselves. These do cause some parties to restructure or abandon deals before filing, but do not show up in the numbers.

Looking at acquirers’ origins, the picture is perhaps surprising: more than half of the completed reviews in 2025 concerned acquirers from the Netherlands itself. Among non‑Dutch acquirers, the United States and neighbouring EU jurisdictions featured most prominently, while filings from Asia or the Middle East remained very limited. This is a point we regularly emphasise to clients: contrary to what the word ‘foreign’ in ‘foreign direct investment’ might suggest, the Vifo Act is not a foreign investment screening regime in any meaningful sense. A Dutch private equity fund acquiring a Dutch dual-use company faces the same filing obligation and the same substantive test as a Chinese state-owned enterprise. The ‘national security’ assessment looks at the consequences of a change of control, not at the nationality of the acquirer as such. However, origin remains a relevant factor in the risk assessment.

From a practical perspective, scope questions remain a recurring theme and, in our experience, dealing with them forms the most time-consuming element of Vifo Act advice. In 2025, several notifications were withdrawn or declared inadmissible because the transaction did not fall within the Vifo Act or the sectoral regimes after all. The Act’s scope extends to acquisition activities concerning companies ‘active in the field of sensitive technology’, but interpreting this concept turns on highly technical questions. Although the BTI has tried to reduce this uncertainty by updating its guidance – in particular by publishing its Dutch-language “actief zijn op” note and additional FAQs, borderline cases remain. Given that the screening process is confidential, early scoping – including an informal view from the BTI – continues to pay dividends for parties navigating the regime.

Finally, enforcement is becoming more visible. The BTI actively monitors for unnotified transactions – contacting companies several times per month based on media reports and other signals – and in 2025 imposed the first “gun-jumping” fine for completing a transaction without prior notification. The stakes are significant: fines can reach €1,100,000 or 10% of annual turnover, and transactions completed in breach of a prohibition decision are null and void. For deal parties, this means that ‘closing quietly’ without a filing is not a viable strategy; we advise clients to treat Vifo compliance with the same rigour as merger control notifications, as the reputational and financial consequences of non-compliance are comparable.

Expanding the screening framework

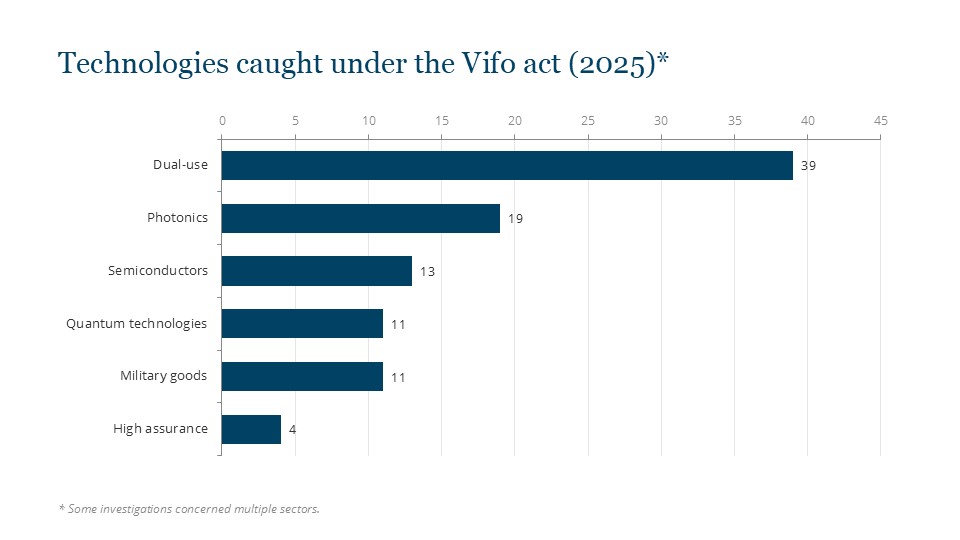

The Dutch FDI-screening framework applies only to investments in certain sectors, with the Vifo Act capturing the vast majority of cases. In 2025, dual-use and photonics represented the most significant sectors, but this picture may change substantially as the Vifo Act’s scope expands.

The scope will be extended (in Dutch) on 1 January 2027 to include six additional fields of very sensitive technology, namely biotechnology, artificial intelligence, advanced materials, nanotechnology, sensor and navigation technologies and finally medical applications of nuclear technologies. The same legislative amendment will upgrade information security and satellite communications from sensitive to very sensitive technologies. This reclassification will lower the jurisdictional thresholds in those areas, bringing smaller stakes and influence increases within scope.

Looking beyond the general regime of the Vifo Act, a sector specific regime for defence and security related activities is on the way. The BTI anticipates that Parliament will receive the Defence and Security-Related Industry (Resilience) Act (Wet weerbaarheid defensie en veiligheidgerelateerde industrie, WWDVGI) in the fourth quarter of 2026. The legislative proposal (in Dutch) would introduce a tailored screening test for defence and security supply chains and empower the BTI to issue suitability declarations to Dutch entities at the request of foreign governments or international organisations.

Whether the BTI can absorb this additional workload is an open question. The bureau – a comparatively small unit – handled 91 screening cases in 2025, yet the sensitive-technology expansion alone is estimated to add roughly 125 cases per year (25 of which are expected to be complex). Once the WWDVGI takes effect, and possibly the Industrial Accelerator Act (which we have reported on before), the actual average review timelines of 37 days (2025) could lengthen materially, adding to deal uncertainty.

Solvinity

On 25 May 2026, acting on the advice of the BTI, the Dutch government prohibited the proposed acquisition of Dutch cloud services provider Solvinity by US-based Kyndryl. Solvinity operates critical digital infrastructure for the Dutch government, including the DigiD platform. Concerns arose that the US government could invoke the Clarifying Lawful Overseas Use of Data (CLOUD) Act to compel access to data held by a post-acquisition Solvinity, even if that data were physically stored in the Netherlands.

Although the Dutch competition authority had separately cleared the transaction from a competition law perspective, the BTI concluded that the acquisition posed a risk to the public interest. The BTI’s advice to prohibit outright rather than impose remedies suggests that behavioural or structural conditions were not considered sufficient to address the identified risks, though the confidential nature of the review means we cannot know for certain.

Note that the prohibition was issued under the Telecommunications Sector (Undesirable Control) Act (Wet ongewenste zeggenschap telecommunicatie, WOZT), not under the Vifo Act. The WOZT applies a broader ‘public interest’ test rather than the Vifo Act’s ‘national security’ standard, illustrating the complexity of the Dutch screening landscape, where multiple overlapping regimes may apply to a single transaction. Moreover, the case shows that even investments from the US – the largest foreign investor in the Netherlands – may now be viewed with greater scrutiny.

Nexperia

Nexperia made global headlines when the Dutch government intervened in the management of the Dutch-based semiconductor manufacturer in October 2025 by ordering a freeze of any significant move of assets or activities. Governance safeguards that had been negotiated since at least 2024 – a supervisory board, reserved matters and a chief security officer – had failed to materialise, and Nexperia’s strategy had increasingly shifted towards a “local for local” model that prioritised securing production in China. Just one day later, the Dutch Enterprise Chamber removed Nexperia’s CEO and placed virtually all shares under a court-appointed custodian. China responded with an export ban on China-made Nexperia products, causing significant disruption to European supply chains and leading the Dutch government to suspend its intervention. The saga continues: in February 2026, the Enterprise Chamber ordered a still-ongoing formal inquiry (enquête) into Nexperia’s conduct and the schism between the Dutch entity and its Chinese parent. Wingtech, the parent company in question, has since filed lawsuits against Nexperia, claiming over € 1 billion in compensation for economic losses resulting from the actions of the Dutch management before the Enterprise Chamber, as well as claims against the Dutch State for close to € 7 billion.

The Nexperia case exemplifies the difficulties of ex-post intervention. Because Wingtech’s acquisition took place in 2019, before the Vifo Act entered into force, the government had to fall back on the Availability of Goods Act (Wet beschikbaarheid goederen) for the first time since its adoption in 1952 in order to effectuate the freezing order described above. This Availability of Goods Act is a blunt instrument compared to upfront screening under the Vifo Act, which is far preferable to intervention after control has already transferred.

European Developments

Revision of the EU FDI Screening Regulation

In June 2026, the European Council approved the text of a revised FDI Screening Regulation. The new rules will apply 18 months from the date of entry into force. The revised regulation makes national screening mechanisms mandatory and sets a minimum scope (including semiconductors, AI, quantum technology, critical raw materials and electoral infrastructure). In addition, it captures intra-EU investments by non-EU controlled entities (closing the Xella gap), and introduces a standardised 45-day first-phase review period. Member States must also provide for a call-in power to retroactively screen transactions that were not subject to prior authorisation.

Deal structures using EU-incorporated acquisition vehicles to avoid screening will no longer be effective. For Dutch targets, the combined effect of the Vifo Act technology expansions, the forthcoming WWDVGI for defence, and the EU-driven harmonisation will increase regulatory complexity.

Conclusion

The shift towards mandatory screening, stricter timelines and consistent treatment of indirect ownership that we flagged in our earlier Competition Outlook is materialising faster than anticipated. The Council vote on the revised FDI Screening Regulation, the first WOZT prohibition and the first gun-jumping fine all confirm that the screening landscape is tightening – not just on paper, but in practice. With the revised FDI Screening Regulation, the WWDVGI and further Vifo Act expansions on the horizon, investors targeting Dutch technology, defence or critical infrastructure assets should treat FDI screening as a first-order deal consideration, not a compliance afterthought.